Weekly Update #17 - Week Ending 05/31/26

$FEIM, $RMB.V, $BQE.V, $FSI, $NSYS, $OGD.TO, $ROMJ.V

Highlights

FEIM (Contracts/Awards): Record $100M backlog, but the stock looks more than fairly valued.

RMB.V (Quarterly Results): Strong revenue numbers, but little of it reached the bottom line. Balance sheet liquidity is the concern, and the M&A playbook will likely slow down.

BQE.V (Quarterly Results): Ugly revenue and EPS on tough comps, but a very clean balance sheet that keeps the company's optionality intact.

The following will cover stocks that are either in our microcap quality indexes (MSMqi) or in our research journal (stocks that don’t quite qualify to be in the MSMqi, but might be close).

Studs (Positive News)

1) FEIM | Precision Timing and Frequency Electronics

Contracts / Awards

FEIM 0.00%↑ announced $16M in new U.S. Government contracts for oscillators and timing systems. Two elements are worth highlighting:

Entry into Space Defense: This award pushes FEI into space defense (countering space-based threats), a brand-new end-market built on its secured-comms heritage.

Strong Backlog: As of April 30, 2026, backlog topped $100M for the first time ever. This is big news because just a few months earlier, FEIM had a backlog of $83M.

Management says that this news raises its conviction in the long-term goal of at least $150M in revenue within three years.

Strong news, but we think the stock is probably more than fairly valued. As laid out in Weekly Update #13, we see FEI generating around $3.26 in EPS by 2029, which puts it at a 22.9x forward P/E. And the risk with FEI is always timing, backlog slipping, rather than converting.

Note: Stock is in our Microcap Quality Index

Duds (Negative News)

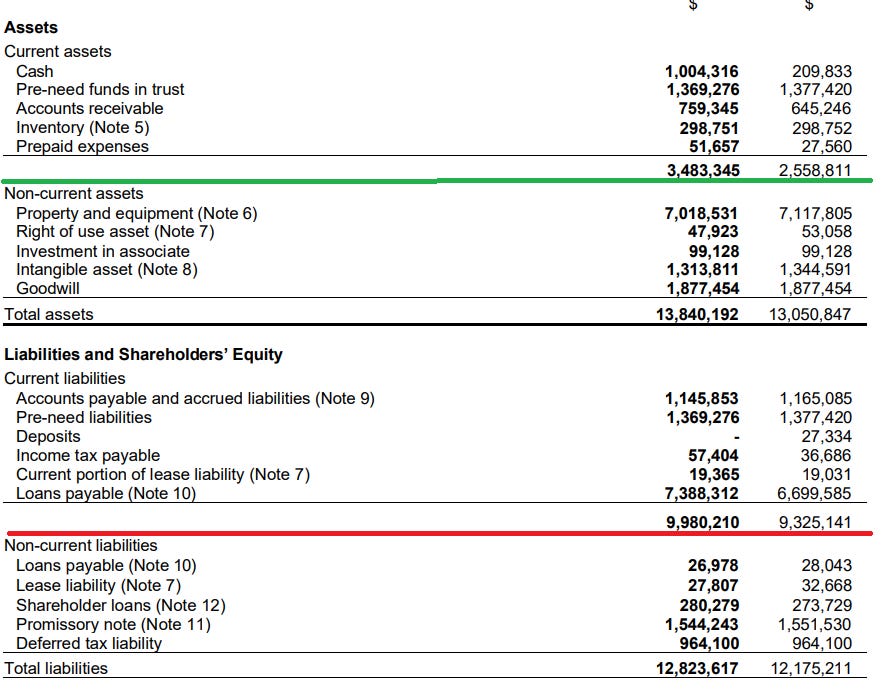

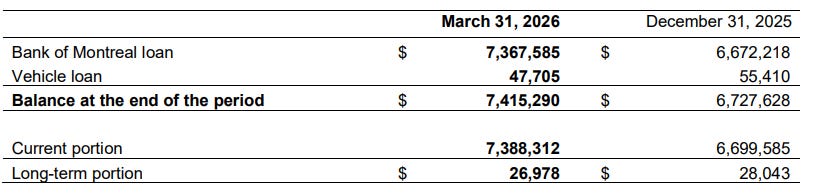

1) CVE:RMB | Funeral Home Operator

Quarterly Results

RMB posted Q1 2026 revenue of $2.4M vs $1.7M in the prior year (+40% YoY), and EPS of $0.01 vs $0.02 in the previous year.

The revenue growth is impressive and was the result of M&A (Reminder: Rumbu is a funeral home roll-up), but this clearly did not flow to the bottom line. The balance sheet is the real problem.

As seen in the image above, the company has 3.48M in current assets against $9.98M in current liabilities. The $7.39M in loans payable is clearly an issue, and they’ll probably have to refinance this debt. With this balance sheet, the M&A playbook will probably have to slow down. If I am honest, I am not usually a fan of companies that do M&A, especially if it’s their only growth engine. This Rumbu situation reminds me a little of LAKE 0.00%↑ .

Note: Stock is in our Microcap Quality Index