Weekly Update #14 - Week Ending 05/10/26

$FTK, $CPH.TO, $MYE, $ACFN, $KE & Others

Studs & Duds, Stocks On Our Radar, and Information Arbitrage TearSheets from companies in our Microcap Quality Index…

Highlights

$FTK (Quarterly Results): Data Analytics grew 295% YoY, Power Tech’s 3-year backlog exceeds $90M, and gives the company Data Center exposure.

$CPH.TO (Quarterly Results): Fully repaid the entire $40M of Natroba acquisition debt in just 20 months. FCF machine with $90M+ of available credit to deploy on M&A.

🔒🔒🔒🔒 (Quarterly Results): Breakout quarter with revenue up 40% YoY and backlog at all-time highs. Tomorrow, we will post an update explaining why we think the stock can double again over the next twelve months and move higher in the long term.

🔒🔒🔒🔒(Quarterly Results): A microcap software name in our Index posted revenue up 73% YoY at a run-rate P/E of 5.0x. The name has a messy capital structure, but we don’t think it’s an existential risk

The following will cover stocks that are either in our microcap quality indexes (MSMqi) or in our research journal (stocks that don’t quite qualify to be in the MSMqi, but might be close).

Studs (Positive News)

1) FTK| Oilfield Chemicals and Data Technology

Quarterly Results

FTK posted Q1 2026 revenue of $70.1M vs $55.4M in the prior year (+27% YoY), and EPS of $0.12 vs $0.17 (-29% YoY, due to a tax normalization ) in the previous year.

The main highlight of FTK is its Data Analytics segment, which grew 295% YoY in Q1, and now accounts for 50% of total gross profit vs just 8% a year ago. The engine behind that growth is Power Tech, FTK's proprietary platform that uses real-time analyzers and gas conditioning equipment to monitor and optimize fuel quality for distributed power generation (e-frac fleets, natural gas power, and increasingly data centers).

The forward pipeline here is interesting: Power Tech's expected 3-year backlog now exceeds $90M, and management called out a 200+ MW pipeline tied to data centers and behind-the-meter power generation they're pursuing into 2027.

FTK is also deploying $10M in new gas conditioning equipment that comes online by mid-2026 and carries ~81% gross margins. Management explicitly said they assumed conservative utilization rates for this equipment when setting 2026 guidance, meaning there's room to beat if demand materializes as expected.

Note: Stock is NOT in our Microcap Quality Index; it’s a Research Journal

2) CPH.TO / CPHRF | Dermatology Focused Pharmaceutical Company

Quarterly Results

CPH posted Q1 2026 revenue of $12.5M vs $12.0M in the prior year, and EPS of $0.24 vs $0.10 in the previous year.

The most underappreciated development is that Cipher fully repaid the remaining $5M on its revolver, meaning the entire $40M of debt drawn for the Natroba acquisition has been paid off in just 20 months. As we've flagged before, Cipher is a free cash flow machine and will probably do some M&A soon.

The main caveat I would point out is that organic growth will most likely not be high and that Natroba revenue has not yet accelerated.

In terms of valuation, Cipher is trading at a 2026 & 2027 P/E of 18.0x - 14.5x, respectively, which is probably fair-cheap, considering the company prints cash and + inorganic growth opportunities. Analyst estimates don’t bake in M&A, so the stock will probably move higher once they announce an acquisition.

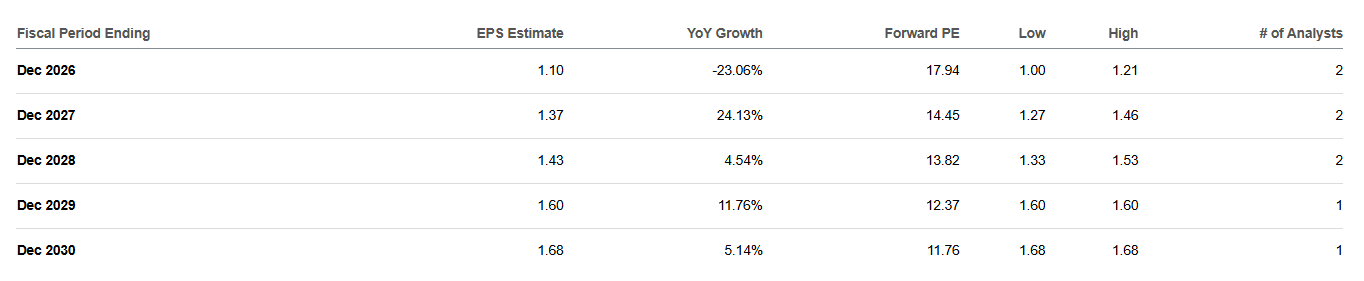

EPS Estimates

Note: Stock is in our Microcap Quality Index