The most Important Weekly Update We’ve Done - Weekly Update #15 - Week Ending 05/17/26

$IFA.TO, $LEAT, $BDT.TO, $HMM.A.TO, $FENC, $BRM.V, $ICCC, $BDCO, $PSIX, $ROMJ.V, $XBP, $FSI, and others.

This week is longer than usual, but it’s a must read for microcap and small-cap investors. Earnings season delivered a record quarter from IFA, Bird's first data center contract win, and new evidence on Hammond's data center exposure. Worth taking your time with this one. This update includes some primary research channel checks on a company that’s downplaying some of their growth opportunities… but our channel checks tell a different story…

Highlights

$IFA.TO (Quarterly Results): Revenue +288% YoY to a record $27.5M, and adjusted EBITDA margin jumped to 21% from 4%. Small Cap Discovery Call indicates 2026 will be a record year.

$LEAT (Quarterly Results): Revenue +27% YoY and net income +58% YoY. Strong outlook for the upcoming quarters, with all major product categories growing.

$BDT.TO (Quarterly Results + Partnership): Record C$5.4B backlog (+24% YoY) plus a partnership with Bell AI Fabric to build Canada's largest purpose-built AI data center.

$HMM.A.TO (Management Call): We believe management downplayed data center exposure on our call, but we found further evidence that proves this exposure is real and percolating.

The following will cover stocks that are either in our microcap quality indexes (MSMqi) or in our research journal (stocks that don’t quite qualify to be in the MSMqi, but might be close).

Studs (Positive News)

1) IFA.TO | Textile Technology Products Developer

Quarterly Results

IFA posted Q1 2026 revenue of $27.5M vs $7.1M in the prior year (+288% YoY), and EPS of $0.122 vs $0.003 in the previous year.

A monster quarter that beat the high end of management's own guidance. However, two days after the print, IFA announced a $25M bought deal (later upsized) at $3.70/share. Although we’re not big fans of dilution, issuing shares at current prices probably makes sense, and the SmallCap Discoveries interview gives us some clue as to why they might be raising this cash:

Scrubs expansion beyond Walmart: The program is “not going to be a Walmart-specific program by any stretch.” The U.S. scrubs market alone is ~$20B; globally it’s ~$60B. The program is also expanding into Canada.

Footwear: The Costco program will repeat in 2026/2027 in “more categories” beyond what was done in 2025. Management strongly hinted that the program will grow meaningfully.

New non-apparel category launching December 2026: A completely new area of business where IFA has never operated before.

Strong 2026 Growth: Management guided to growth of at least 50-60% for 2026, although Atrium expects 94% growth.

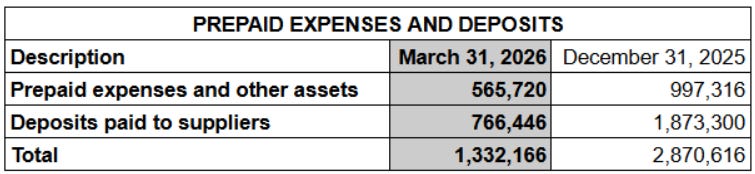

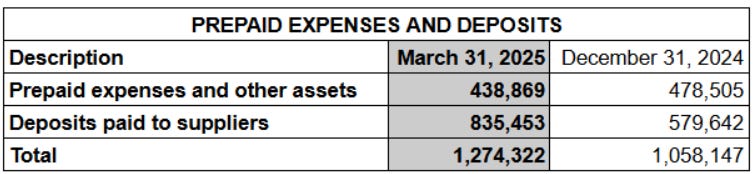

The only negative thing I’d point out is that deposits paid to suppliers, which are the leading indicator for Ifabric sales, are down YoY. However, their inventory remains elevated (despite this monster quarter). This most likely implies deposits will build up over the upcoming quarter.

Although the stock is definitely not as cheap as when we flagged it in Cliff Note #126 at C$1.21, it does seem like Ifabric has a significant growth runway and can probably double by 2027.

Note: Stock is in our Microcap Quality Index

2) LEAT | Protective Gear for Motorsports

Quarterly Results

LEAT posted Q1 2026 revenue of $19.5M vs $15.4M in the prior year (+27% YoY), and EPS of $0.28 vs $0.18 in the previous year (+56% YoY).

When we added the stock to the index about a month ago in Cliff Note #140, the thesis was pretty straightforward: an industry emerging from a four-year industry destocking cycle + a company with strong operating leverage.

Although I have to admit that I feared Q4 growth would slow down, this strong Q1 eased my concerns. Management even mentioned:

“We expect working capital investments to grow in the coming periods as ordering patterns continue to signal growth, and we have sufficient liquidity to fuel this growth.”

Overall, I think this was a good quarter, and think the stock is still cheap since it’s trading at a run-rate P/E of 10.8x.

Note: Stock is in our Microcap Quality Index

3) BDT.TO | Construction and Infrastructure Contractor

Quarterly Results

BDT posted Q1 2026 revenue of C$783.4M vs C$717.6M in the prior year (+9.2% YoY), and adjusted EPS of C$0.25 vs C$0.23 (+8.7% YoY).

The bigger news was that Bell selected Bird as the lead construction partner for its 300 MW AI data centre in Saskatchewan and formalized a long-term strategic partnership for Bell’s multi-year, Canada-wide AI data centre buildout. This is Bird’s first disclosed data center contract win. Bird is now Bell’s preferred construction partner nationally. Bird had been hinting at data center opportunities for several quarters, and this opportunity is now coming to fruition.

Bird is trading at a 2026 P/E of 22.8x, so it’s not exactly cheap; however, it looks much more reasonably valued on 2027 numbers (15.9x P/E).

Can it re-rate further? I think so. Other peers with meaningful data center exposure are trading at P/Es above 30.0x, and Bird also has some defense + nuclear exposure.

Note: Stock is in our Microcap Quality Index

4) HMM.A.TO | Electrical enclosures and racks manufacturer

Management Call

Last Friday, we had a call with Hammond Manufacturing’s management team, and the results were quite unexpected. We think management downplayed the data center angle on our call; however, we found further evidence that shows the exposure is very real.