Shorting Microcaps Without Getting Killed

A field guide for retail investors who avoid the short side, because nobody ever explained how it actually works

What follows is a contributory educational article on “short selling” from a Subscriber & research contributor to our Microcap Investing Cliff Note Substack and Geoinvesting. You should definitely follow him at his Substack, Macro Mind, Micro Market. His analytical skills are awesome, and he’s definitely a stock picker you want on your team.

Enjoy!

Shorting Microcaps Without Getting Killed

A field guide for retail investors who avoid the short side, because nobody ever explained how it actually works

Most of what’s written about short selling is a victory lap. Someone caught a fraud, rode it to zero, and wrote it up afterward as if the hard part was being smart. For small and microcap stocks, that gets the difficulty exactly backwards. The hard part is rarely spotting that something is overvalued, as the market is littered with overvalued junk. The hard part is everything that happens between “this is obviously worth less” and “I actually made money being right.”

This piece is for the investor who has looked at a promotional microcap trading in fantasy land and thought “I should be short this” — and then, sensibly, didn’t, because the mechanics were a black box. I want to open the box. By the end, you should understand why most microcap shorts are untradeable, how to recognize the few that aren’t, and why the answer to “should I short this?” is usually no, by understanding exactly which part of the plumbing stops you. A quick definition for anyone new: shorting means borrowing shares, selling them, and hoping to buy them back cheaper to return them. Your profit is capped (a stock can only fall to zero), and your loss is theoretically unlimited (it can rise forever). That asymmetry alone should make you cautious. In microcaps, it gets worse, and understanding why is the whole game.

There are really only two ways to act on a bearish view, and they answer different questions. You can try to hedge, that is, protect yourself from a broad small-cap downturn during a market sell-off, or you can bet against a specific company. People constantly mix these up: they get a vague “this whole market is frothy” feeling and try to express it by shorting one stock, or they have a sharp single-company thesis and reach for a blunt market hedge. The two don’t substitute for each other, and seeing why is half the education. Let’s take them in order.

Can you just hedge it instead?

A natural first instinct: rather than short individual scary names, why not buy something that goes up when small caps go down? The popular tool is an inverse ETF like RWM (which is built to deliver the opposite of the Russell 2000’s daily move — note you buy it to be bearish, you don’t short it).

It’s not a crazy idea, and its fans make a genuinely good point: when you’re wrong, your losing position gets smaller, not bigger. If you short a normal ETF and it rises, your loss grows and can squeeze you. An inverse ETF is just a thing you own — it can’t lose more than you put in, and it automatically shrinks its exposure as it falls. That’s real, and it’s a true advantage over shorting outright.

But that same advantage is the source of its biggest flaw. Inverse ETFs reset every single day, and that daily reset quietly bleeds you in choppy markets — a phenomenon called volatility drag. The mechanism that shrinks your loss in a steady decline is the same mechanism that grinds your capital away in a market that chops sideways. Up 10% then down 10% leaves the index roughly flat, but leaves the inverse ETF down. Small caps are nothing if not choppy. These products are built to be held for days, not as a standing hedge.

There’s a deeper problem for true microcap investors searching for companies under a $500 million market cap with unique risks: the Russell 2000 isn’t your universe. It’s a small-cap index, and its average company market-cap dwarfs the genuinely tiny names in your portfolio you are trying to protect. The risk that takes your face off in a concentrated microcap book is idiosyncratic — one company’s surprise dilution, one fraud, one delisting — and none of that lives in a broad index. You can take a brutal single-name hit on a Friday-night capital raise while the index is green. A broad-index hedge protects against the wrong risk.

“Just use a microcap ETF then” (IWC) runs into a wall: it’s a fraction of the size and liquidity of the big small-cap funds, and — critically — it has essentially no usable options market. And “just buy put options” runs into another: options decay (you pay theta, the daily rent on an option), and microcap-flavored options are expensive precisely because the stuff is volatile. You buy fire insurance in the arson district at arson-district prices.

Here’s the unifying lesson, and it’s the one that carries into the rest of the post:

There is no carry-free way to hold a position against the market. Every hedge charges rent — it just differs in form. Inverse ETFs charge volatility drag. Outright shorts charge borrow fees and uncapped risk. Puts charge premium and decay. You don’t get to avoid the rent; you only get to choose which rent matches your situation.

The main takeaway is that you can’t fully hedge a concentrated microcap book with an index. You can buy disaster insurance against an asset-class-wide liquidity event, but idiosyncratic risks like the single-name dilution print have to be managed by position sizing, not hedged away. Which brings us to the harder question.

The real game is alpha, and it has three gates, not one

If you’re going to bet against a specific company, the trade has to clear three gates, not the one most people stop at.

Gate 1 — Is it overvalued? This is the easy one, and I want to be blunt: this is table stakes, not edge. Anyone can find a company trading at a silly valuation. If your entire thesis is “this is too expensive,” you don’t have a trade yet.

Gate 2 — Is there a catalyst with a clock? What specific event forces the price to resolve, and when? “It’s overvalued” has no date. “Their cash runs out in Q3” or “the lockup expires in March” does. And add a durability sub-test that saved me a lot of pain, only after it cost me a lot: ask what reverses the catalyst. A debt maturity can be extended. A pundit’s negative comment can be walked back. A confirmed-dead acquirer cannot be unconfirmed. The more reschedulable your catalyst, the softer your trade.

Gate 3 — Can you actually implement it? This is the gate retail never hears about, and it kills more good theses than bad analysis ever does. Can you borrow the shares, at a tolerable fee, without getting recalled? Is the margin requirement survivable? Is there enough liquidity to get in and out? Do options exist if you’d rather define your risk? A thesis that fails Gate 3 isn’t a worse short — it’s a non-short, a watchlist item until the plumbing changes.

A short seller I respect, Sean Westrop of Deep Sail Capital, put the scale of Gate 3 vividly in a conversation that shaped a lot of this piece: of a hundred obviously-bad companies he could name on the spot, only six or seven actually clear all the implementation hurdles enough to short. Finding the junk is easy. Finding the junk you can trade is the job.

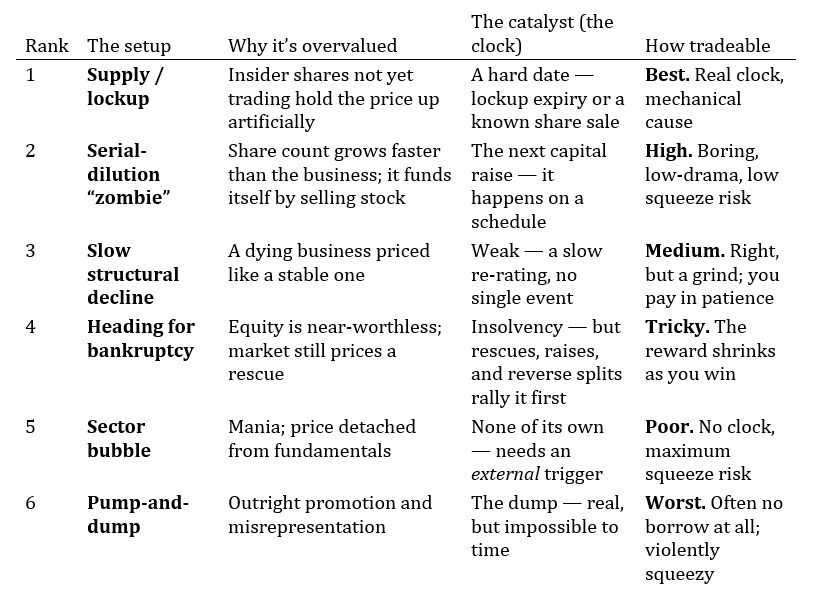

The six kinds of microcap short, ranked by how tradeable they are

Here’s the part that reorders most people’s intuition. Below are the six setups, ranked not by how outrageous the company is, but by how good the catalyst is and whether you can actually put the trade on. Outrage is not edge.

Notice what the ranking does: the dramatic shorts, such as the bubble, the pump, the imminent bankruptcy, sit at the bottom. Not because the theses are wrong, but because their catalysts are absent, external, or untimeable, and they’re the hardest to actually trade. The boring, mechanical, supply-driven shorts at the top are the ones that pay. A skeptical reader instinctively ranks these by fraud and fireworks; the table inverts that on purpose. The flashy shorts are where short sellers go to be right and get squeezed anyway.

Two refinements worth keeping in your head, both learned the hard way:

The crowded-short trap. Once a stock is branded a “shitco,” it can carry very high short interest for years — and people keep shorting it simply because everyone else is. That crowding is squeeze fuel, and occasionally the company quietly turns around while the bears are still piling on. High short interest is as often a warning to your short as a confirmation of it.

Bubbles don’t deflate on a schedule. The clean ones (the 2022 EV bubble — Rivian, Lordstown, and friends; the earlier 3D-printing bubble) followed a tidy pattern: peak, sharp drop, flat, then a slow multi-year grind lower. You short the lower highs, not the waterfall. But some bubbles have a live, powerful sponsor and refuse to behave, which I learned painfully, below.

Can you even put the trade on?

Let’s make Gate 3 concrete, because it’s where retail gets ambushed.

Borrow fee: the annualized cost of borrowing the shares to short. On a hot microcap, this can be 30%, 80%, or — I’m not exaggerating — into the hundreds of percent. A correct call can be a losing trade purely on carry.

Recall: the lender can demand the shares back, forcing you to buy in at the worst possible moment.

Margin requirement: separate from the borrow fee, this is how much capital the position ties up. On a small, illiquid name, it can be punishing — I once wanted to short a well-researched name (a short pick at Maj’s Active Portfolio Substack that, for the record, did fall as they predicted) and the margin requirement was roughly 10x. Tying up ten units of capital to short one unit, for a target gain of maybe 30%, is a non-starter no matter how right you are.

Liquidity and options: can you size in and out without moving the price, and is there an options chain to express the view with defined risk?

When the borrow cost or the margin blocks the obvious approach, two tools can sometimes unlock it — but neither is free; each just swaps one risk for another (the rent law again):

Options and put spreads relax the borrow/squeeze problem. A put can’t be recalled and can’t lose more than you paid, so the squeeze that destroys a naked short just expires the put. You don’t escape the borrowing cost, though — it’s baked into the option’s price. And a put spread (buy one put, sell a cheaper, lower one) deserves special mention, because it pairs perfectly with a fact Sean stressed: the realistic target for a short is about a 30% drop, then you cover, not zero. Riding to zero happens maybe a handful of times in a career. If you’re not riding to zero, you shouldn’t pay for zero — so sell the lower strike, finance your trade, and cap a profit you weren’t going to collect anyway.

Pair trades relax the margin/directional problem: short the weak company and go long a quality peer, so a market rally doesn’t run you over, and (on the right margin setup) the long position reduces the capital the short ties up. The catch is a paradox every long-short investor eventually meets: in a rally, the junkiest stocks run the fastest (bears covering, crowded shorts unwinding all at once). So the pair can move against you on both legs precisely when you’re losing. It’s the right tool for a relative-value “this deserves a lower multiple than the leader” thesis, and the wrong tool for a binary collapse, where you don’t want to be long anything.

, which tool relaxes it (teal), and the new risk you swap in — with the dead-ends in red where the gate simply shuts.")

The implementability gate. Which constraint binds (the amber decisions), which tool relaxes it (teal), and the new risk you swap in, with the dead-ends in red where the gate simply shuts.

The decision logic, in plain form:

Borrowable, cheap, not squeezy? Short it outright. Cheapest expression wins.

Squeezy and hot borrow, but a real options chain exists? Use a put spread.

A relative-value laggard, not a binary? Consider a pair against the quality leader.

True microcap, no borrow, and no options? There is no good instrument. Watch it, or — if it’s a low-float rocket — recognize that the better trade might be a long squeeze, not a short.

That last line is the salient punchline of the whole section: for a large chunk of the microcap universe, the best short instrument is “none.” That’s not defeatism; it’s the single most money-saving sentence in this post.

Four trades from my own book

Theory is cheap. Here are four of my own shorts — two that worked, two that didn’t — chosen because they hold almost everything constant and vary the one thing that decided the outcome: catalyst durability and exit discipline.

The two that worked

iRobot (IRBT) — the death short. The thesis was hard and confirmed: the last potential acquirer had walked away, bankruptcy looked imminent, and common shareholders would be wiped out. I shorted it outright but bought cheap, far-out-of-the-money call options as protection against the one thing that kills a death short: a sudden squeeze. When the squeeze came, I sold the calls into it (their value spiked exactly when I needed it), then rode the unprotected short down. I covered for a large profit when the stock was delisted. The structure here — naked short plus a cheap call overlay — is better than a put for a genuine ride-to-zero conviction: you keep the entire descent, pay no decay on the core, and insure only the squeeze. Just remember that riding all the way to delisting is the rare exception, not the base case.

Sidus Space (SIDU) — the zombie. I knew this company’s pattern: it dilutes — sells new stock — into every rally. So I expressed a bearish view with puts (defined risk, so a rip couldn’t take me out while I waited), let the known, recurring catalyst do the work, and closed for a profit after the next dilution hit. Nothing about it required predicting zero. It’s the boring #2 setup played exactly to spec, and it’s far more repeatable than the dramatic IRBT win.

The two that didn’t

Funko (FNKO) — the soft catalyst. I thought it was the next IRBT: heavy debt with a repayment wall looming, and a weak toy market (Mattel had just missed badly). But I made three mistakes. First, I pattern-matched IRBT’s ending without checking that FNKO shared IRBT’s load-bearing fact — and it didn’t. IRBT’s acquirer was confirmed gone; FNKO’s debt wall was merely a deadline, and the company simply extended it by a year (an “amend-and-extend” — the maturity moves, the leverage stays). A reschedulable deadline is a soft catalyst, because lenders usually prefer extending to forcing a default. Second, “the toy market is weak” is a sector read — beta, not a clock. Third, and worst: I went naked on my weaker thesis, having correctly hedged my stronger one (IRBT). My protection was inversely related to my conviction. The extension bought the company time, activists engaged, it beat estimates, and I covered at a real loss.

IonQ and Rigetti (IONQ, RGTI) — the reversible catalyst, and no exit. I got almost everything right. I correctly identified the quantum-computing names as a bubble, I correctly timed my entry to a moment of broken momentum (a prominent industry figure publicly dismissed quantum, and the stocks dropped ~30%), and I correctly used puts on liquid, high-volatility names. My single mistake was that I didn’t take the 30%. I held for the conviction that “the trend is finally broken.” In a bubble with a powerful institutional sponsor, no single comment confirms a structural break — the drop was a dip, not the top — and the catalyst then reversed when that same figure pivoted to embracing quantum. Holding outright puts through a reversal is doubly punished: decay while you wait, and the rally crushes the premium. I covered at a loss. A put spread would at least have enforced the exit; the deeper fix was simply to take the win.

The rules that fall out

Lay the four side by side, and three rules appear — and the nice thing is they’re proven by my own P&L, not asserted:

Wins ran on hard or recurring catalysts; losses ran on soft or reversible ones. Always ask: what reverses this?

SIDU and IONQ are the same instrument (puts) with the opposite discipline. On one, I took the ~30% and left; on the other, I overstayed for a structural dream the market wouldn’t honor. Take the 30%.

FNKO and IRBT show that protection should scale inversely with confirmation. The less confirmed your binary thesis, the more you need defined risk. Earn the naked short with confirmation, not with conviction.

Where I find shorts (and thank-yous)

A lot of the implementation realism in this post — the “six of a hundred are tradeable” filter, the 30%-target discipline, the way bubbles deflate — came from a conversation with Sean Westrop of Deep Sail Capital (@DeepSailCapital), who writes the Shorts & Squeeze Corner Substack. Where his framing did the heavy lifting, I’ve tried to say so. The instrument engineering on top of it — the pair-trade and put-spread mechanics, the call-overlay death short — is my own, as are the four trades and their bruises.

That conversation was a “skull session” that Maj Soueidan invited me into at his Skull Sessions Substack — my thanks to Maj for the seat at the table, and for running the kind of microcap community where this gets talked through in the open. And separately, I owe Florian Buschek, who writes Breakout Investors, for flagging the structural cracks at iRobot to me well before that short became obvious.

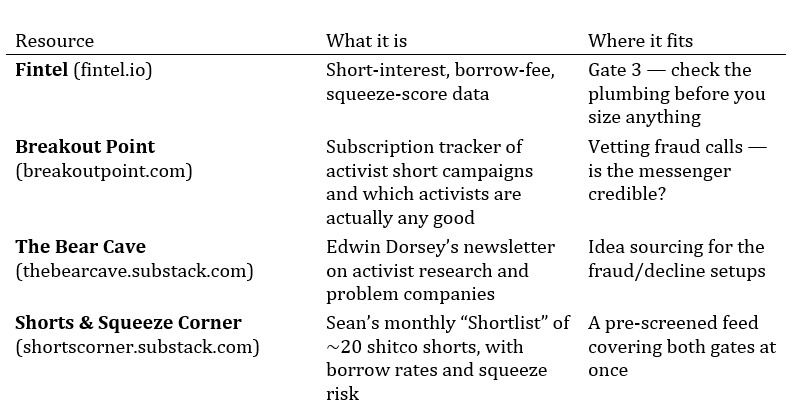

The tools I actually use, mapped to where they help:

Beyond the tools, it’s worth following the established activist short-research shops directly on X, where the reports — and the market’s reaction — break in real time. A non-exhaustive starter list: Muddy Waters Research (@MuddyWatersre), Spruce Point Capital (@sprucepointcap), Kerrisdale Capital (@KerrisdaleCap), Culper Research (@CulperResearch), Bleecker Street Research (@Bleecker__St), and Fuzzy Panda Research (@FuzzyPandaPA) — plus Sean’s own Deep Sail Capital (@DeepSailCapital).

One habit matters more than any of these accounts: read the disclosure at the bottom of every report. These firms are almost always short the stock they’re writing about, and most state outright that they may cover their position — possibly all of it — at any time, including right after publishing. That doesn’t make the research wrong; their incentive is to find real problems. But it means a report is the start of your own work, not the end of it, and that violent first-day drop is often where they are taking profits, not where you should be jumping in.

The bottom line

If you came here hoping to be talked into shorting microcaps, I’ve probably done the opposite, and that’s intentional. The reason most retail investors avoid the short side isn’t ignorance to be cured — it’s a reasonable instinct. Shorting microcaps means a capped gain against an open-ended loss, in the least forgiving corner of the market, where being right and being early are indistinguishable on your statement, and the carry runs the whole time you wait.

What I hope you take away isn’t to go short — it’s to understand the machinery. Know why the index hedge doesn’t protect you. Know the three gates. Know that the boring supply-driven shorts beat the dramatic ones. Know that for most names, the answer is “you can’t, cleanly” — and when you can, that defined-risk structures (puts and spreads) exist precisely so you can be wrong without being destroyed. That knowledge makes you a better long-term investor, too: every short setup above is a list of red flags to keep you out of the wrong longs.

This is a write-up of my own experience and analysis for educational purposes. It is not investment advice, and I’m not your advisor. Short selling carries the risk of unlimited loss and is especially dangerous in small and microcap stocks. Do your own work, and size accordingly — or don’t play.

I agree. And the market got much more sentiment driven that makes it more difficult to time the right short.

Great job on this. One thing that is worth noting is that regulators seem to care less about stepping in when there is fraud vs. when I was shorting stocks between 2010 and four 2014. This also increases the risk of being short.