Research Pipeline Session #20: A Mispriced Industrial With an Unrecognized AI Business

An Industrial wrapper hides a capital-light, 50%-growth data center component business

On its own, a capital-light data center power business growing ~50% YoY would trade at 5–7x EV/Sales. Inside a loss-making industrial wrapper dominated by operational setbacks in the legacy segment, the same business is being valued at a fraction of that. A SOTP using sub-tier AI-component comps, heavily discounted for sub-scale and unproven 800V positioning, still leaves meaningful upside.

As a reminder, Research Journals contain ideas that are part of our pipeline. These ideas are not yet in the Microcap Quality Index (MSMqi), but they have the potential to graduate into the index over time. It gives you early access to stocks that may have moved up our research pipeline.

Some recent examples of strong performers that have moved from our Research Journal pipeline into the Index include:

Within this post, we discussed how you could’ve easily found the information arbitrage.

Note: You could’ve definitely caught this name by checking out the company’s latest d-sheet (Press Release vs Conference Call Comparison):

Methode Electronics Inc (NYSE: MEI)

1) Company Overview

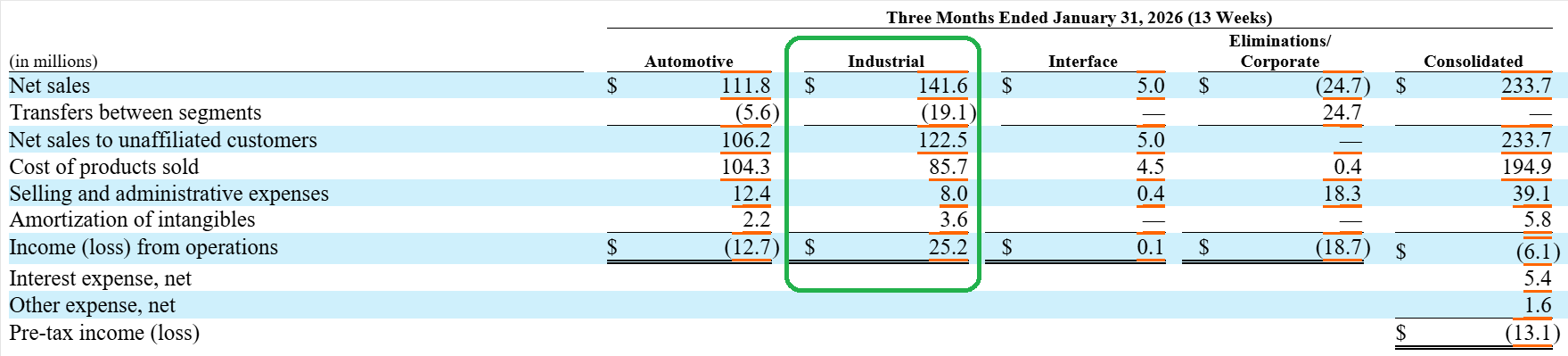

What they do: Custom-engineered electronic and power-distribution components (switches, sensors, lighting, busbars, cabling) sold to manufacturers on multi-year programs. $980M in TTM revenue, but profit comes almost entirely from the Industrial segment.

Segments:

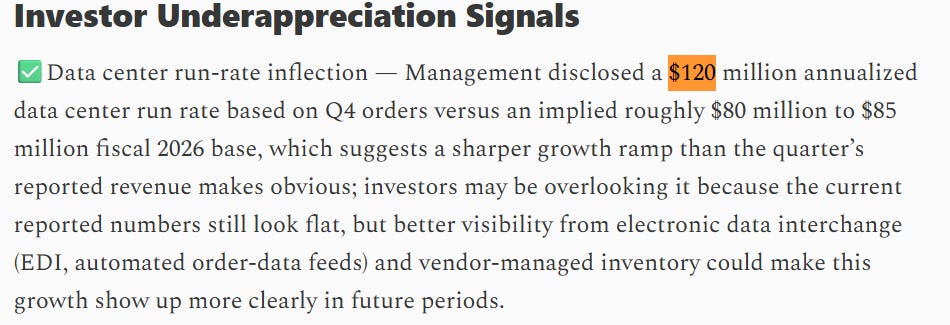

Industrial ($490M): Lighting, remote controls, and power-distribution hardware; contains the hidden $120M data center business. Clients include data center CMs, off-road/construction equipment, and aerospace/defense.

Automotive ($430M): Consoles, switches, sensors, EV/hybrid power content; loss-making, shrinking, concentrated in North America. Clients are auto OEMs and their suppliers (e.g., Stellantis program).

Interface ($25M): Data-over-copper and appliance touch panels; tiny and shrinking. Clients are appliance and networking customers.

2) Reasons to Track

2.1) Strong Industrial Segment: MEI’s Industrial segment is literally generating all of the company’s operating profit; however, it is masked by the substantial losses of the automotive segment.

In its latest 10Q, the company specifically states this segment is exposed to the aerospace, data center, power conversion, and military telecommunications markets.

2.2) Hidden DC asset inside a distressed wrapper: As previously mentioned, MEI has DC exposure through its industrial segment. If we check the company’s CCs, we can see that this segment has been growing rapidly. Check out the revenue numbers:

2023 (FY Ends in May): $25M

2024: $41M

2025: $80M

2026: $80M

2027 (Management Guidance): $120M run-rate

The data center power business is at $120M in run-rate revenue, growing 50% YoY; however, it’s invisible because it sits inside MEI’s industrial segment.

According to management, the core product of this DC segment is busbars, laminated copper bars that carry high current between points in a rack, and they’re essential to data centers because, as AI workloads push rack power densities past 100kW, traditional cabling can no longer move that much current efficiently.

The DC business is capital-light, and management has explicitly stated that no material CapEx has been deployed into this business. They’re growing this through existing capabilities and a vendor-managed inventory (VMI) model, meaning that MEI holds and manages the inventory at the customer’s location, replenishing it based on real-time usage data the customer shares electronically (EDI). The customer doesn’t place traditional purchase orders; MEI sees consumption and ships against it.

This is important for two reasons.

First, it makes MEI stickier, once embedded in a customer’s planning systems and physically stocking their facility, switching to a competitor becomes operationally disruptive, not just a procurement decision.

Second, it gives MEI better demand visibility, which is why management feels confident enough in the $120M exit run-rate to disclose it as “EDI-backed” rather than a contract estimate.

2.3) New management + self-help levers: Entirely new team installed mid-2024. CEO Jon DeGaynor (ex-Stoneridge CEO, directly analogous auto/CV electronics background), plus new heads of automotive, strategy, and procurement. Since taking over, they’ve sold dataMate ($16M), agreed to sell the Harwood Heights facility, cut CapEx from $42M to $17M, halved the dividend to preserve cash, amended the credit agreement to stay covenant-compliant, and rolled out EDI-based forecasting and VMI in the DC business.

3) Valuation

Valuing MEI is a little challenging because the only way we can appropriately reflect the value of the DC business is through a SOTP valuation, which I am not a big fan of because management has not indicated it will spin off or give better disclosure on the DC business.

Automotive, Industrial (excluding the DC business), and the interface segment generated $814.8M in sales this last quarter. If we use a 0.7x Sales multiple for the whole company, this means these are worth $570.4M

The DC business will generate at least $120M in sales. Big peers like BELFA and NVT are trading at 5-7x sales. Although, to be conservative, we can use 3.0x sales, meaning this segment is worth $360M.

This means the whole business is worth around $930.4M, taking into account the net debt and the shares outstanding, which translates to a share price of $19.66. However, we cannot neglect the risks

4) Risks

4.1) Value-realization path: There’s no obvious mechanism to force the DC business into the open: no announced spin, no segment re-disclosure, etc.

4.2) Auto is an active cash drain: The automotive segment has run-rate operating losses of more than $50M, and management’s own Mexico-plant turnaround has slipped for multiple quarters, and management actually cut down EBITDA guidance due to auto weakness.

4.3) The DC business is probably a commodity: Busbars, power cabling, and connectors are essential to data centers but contestable. Multiple suppliers can make them, and the named primes (Delta, ABB, Eaton, Vertiv, Schneider) vertically integrate these components in-house. Method itself admits “de minimis” share and sells through contract manufacturers rather than directly to hyperscalers.