Q2 Earnings Review - TSSI

Q2 Earnings Review - TSSI

We currently have 96 stocks in our MS Microcap Quality Index (MSMqi). So, earnings season is going to be getting a little crazy. We start with TSSI.

We currently have 96 stocks in our MS Microcap Quality Index (MSMqi). So, earnings season is going to be getting a little crazy. 🤯

With the Q2 2024 earnings season just about over, I’m going to do a quick Cliff Note-style review on about 20 companies worth talking about the good, the bad, and the ugly. So look for that premium post soon.

But this morning, I wanted to quickly highlight TSSI’s surprise Q2 2024 earnings report released yesterday after the close.

TSSI, a data center integration company, is the second-best performer in our MSMqi, clocking in a return of 450% in 4 months since we published our Cliff Note. I predict TSSI will quickly take the number one spot, maybe today, unseating HMDPF, a manufacturer of transformers. HMDPF Is sitting at a return of 529%, after peaking at over 700% a few months ago. I also think TSSI has the chance of being our first 10-bagger since launching the MSMqi in February 2022. 🤞

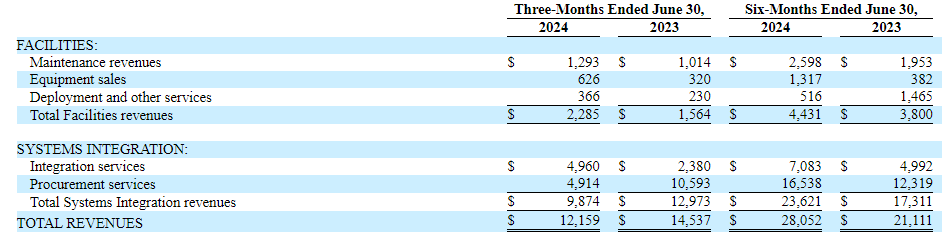

Here is what you need to know: after years of stagnant growth in systems integration revenue, the company finally delivered strong revenue growth in this higher-margin business segment, which has primarily built and delivered racks for traditional (enterprise) data centers in a building. This revenue was up 113% to $5 million and carried gross margins of 43% for the quarter.

The company reported earnings per share of 6 cents versus Q2 2023 EPS of 1 cent. These numbers were clear quarterly records for the company’s systems integration business. Overall gross margins were 36% versus 22% last year.

The growth in the systems integration business was fueled by the company’s backlog of AI integration work, which began to materialize in June.

Overall Q2 sales came in at $12.2 million versus $14.5 million. Investors who are not familiar with TSSI will not understand that the headline number doesn’t tell the whole story.

Remember, as outlined in our Cliff Note, the reseller/procurement business can be lumpy. This is basically revenue generated from its OEM customer (Dell), asking TSSI to procure hardware/software that Dell does not sell but its customers want. It’s a low gross margin business (we estimate around 10%), but it strengthens TSSI's relationship with OEMs. It also opens the door for TSSI to develop closer relationships with customers so that it can possibly perform higher margin system integration services for them. One thing to keep in mind is that even though this business is a low gross margin business, it’s a high revenue business, and a good deal of the gross margin flows right to the bottom line. This quarter, the segment produced income of $600,000.

Investors who have been following TSSI understand that the near-to-midterm growth story and the impetus for valuation multiple expansion to occur revolves around its ability to grow its systems integration business. This is pure data center work. Up until Q2, there has been no dramatic growth in rack integration. All we had was a very lumpy revenue stream in the reseller business here and there. It’s tough to value a business on that type of revenue stream.

Now, recall that in the last few earnings calls, management has said that they have positioned the company to be able to grow the rack integration business by 10x. We are finally getting a glimpse of the type of profitability the company can experience as it grows the system integration business. In fact, on the earnings call, I asked the CEO if efficiencies will improve as the company scales. He very confidently said yes.

It’s going to be interesting to see how earnings per share will play out as the company gets closer to the 10x capacity goal. Prior to this quarter, I had estimated that EPS could reach at least $0.20 per at full capacity. Now, I think that’s potentially conservative. Regardless, it looks like it won't be long until the company is approaching an annual EPS run-rate of $1.00 per share.

I’ll let you decide what P/E to throw on that.

There was another very important takeaway from the earnings call. Management already indicated that they’re going to need more capacity heading into 2025. So, that’s giving us a clue that our $0.20+ EPS assumption could be right around the corner and that 2025 should be a banner year for the company. To accommodate for this growth, management said that it’s eyeing up moving into a new facility to meet demand. Why is this important?

It’s been pretty much assumed that the company's current facility is “dedicated” to its “large OEM customer”, partly because the OEM has actually invested money into the facility. So, we think moving into another facility will allow TSSI to more aggressively expand outside its large OEM relationship and reduce that very large customer concentration risk.

I should add that we think that the company now meets the minimum shareholder equity requirement for an up-listing from the OTC.

Longer-term, two other sources of revenue could help add to and diversify TSSI’s growth.

Modular data centers

Modular data centers are built at a facility and delivered to the customer’s location, typically outside. This option is easier for a company to plan/expand than with an enclosed data center. Traditional data centers that are enclosed require more pre-planning in terms of deciding how big of a building to build to accommodate imprecise expansion needs over time. Modular centers are lighter, customizable, smaller, quicker to deploy, require less equipment, can be more energy efficient, and can be located closer to the processing “edge.”

The company spent some time on the Q2 2024 call talking about how this opportunity is starting to shape up…

“In our modular data center business, while we've seen year-over-year improvement, we're now engaged in promising discussions with prospective customers. Our focus is on building a solid backlog to fuel revenue growth in 2025 and beyond.

We're observing increased refresh activities in existing installations, though new builds are taking longer, particularly for AI solutions due to high GPU demand and anticipated technology releases. In the long term, we see potential synergy between AI and modular form factors, especially for use cases like autonomous vehicles and other time-sensitive applications in underserved areas.”

Facilities Management

This segment provides maintenance services and hasn’t been a consistently big driver of revenue, although it has grown this year, including 44% in Q2 to $2.3 million. This is an area of the business I need to dig into because it carries gross margins of over 70%. I’m not quite sure how the revenue moves with the rest of the business, but it currently appears to be only tied to modular business, which is why the company wants to step up its plans to grow the modular business. So, my original assumption that this revenue would automatically go up with the system integration business was incorrect, although I would not rule out management seeking out ways to expand that business to its system integration business.

What we now know is that getting the modular business growing could be extremely additive to our quarterly EPS run-rate of $0.20+.

Here’s a breakout of the revenue in all of the company’s segments outlined in the Q2 filing:

The gross margin breakout is provided in the management, discussion, and analysis section of the Q2 filing.

Caveats:

Revenue, especially the reseller business will be lumpy. For example, on the Q2 call, management indicated that Q3 will come in at $50 million.

How will the company pay for purchasing/leasing another facility to expand in 2025?

I hope you enjoyed this review on $TSSI. If you found this useful, please consider supporting our movement to create the largest hunting ground for Tier One Quality Microcaps and high-probability turnaround microcaps.

Our MSMqi currently holds 96 stocks and we typically add about three new stocks a month, with a research cliff note. Our multibagger hit rate is also roughly 33%. Therefore on average, add one multibagger per month :)

I was late to the party from your inclusion in the index... but not too late for this Qs results. Looking forward to further progress.