[NEW + FREE] Cliff Note #144 - GETB.L: One Segment Worth Twice the Whole Company + Incentivized Management

Multibagger Factors: Recurring Revenue - SOTP Discount - Incentivized Sale - Strategic Buyer

As we said in a Substack note a couple of weeks ago, our next two investing Cliff Notes (#143 & #144) would be unlocked and free. Cliff Note #143 was TPC, and now we are publishing this new free cliff note, featuring Getbusy plc (LON: GETB), a company with a hidden gem with a segment worth more than the company’s EV.

GetBusy (LON:GETB) is a £37m UK micro-cap that owns a fast-growing US tax-document platform (SmartVault, $18.5m ARR) that’s worth roughly twice the whole company’s enterprise value on its own, even at half the multiple Thomson Reuters has paid for comparable assets.

You get a second profitable business for free, two incentive plans paying management to sell SmartVault and distribute the cash by 2028, and a controlling family buying stock above today’s price.

Data

Symbol: LON:GETB

Founded: 2017 (GetBusy plc; demerged from Reckon Ltd, est. 1987. SmartVault founded ~2008, Virtual Cabinet older still).

Website: https://www.getbusyplc.com/

Price: £0.73

Diluted Shares Outstanding: 50.69M

Market Cap: £36.7M

TTM Revenue: £22.1M

LT Debt: £2.6M

Current Portion of LT Debt: £369K

Cash: £2.5M

P/E trailing 12 months: N/A (losses)

EV/TTM Sales: 1.67x

Insider Ownership: 30.0%

Company Overview

GetBusy is a UK-listed vertical SaaS group selling document workflow and compliance software to regulated professionals such as accountants and tax preparers. Around 97% of revenue is recurring, and because subscriptions are billed a year in advance, working capital is a source of cash rather than a drain. It raised £3m at its 2017 IPO and has not raised equity since, growing in an essentially cash-neutral way.

The group’s near-breakeven result is deliberate: one segment (Workiro/Virtual Cabinet) is run for cash at a 30% EBITDA margin, while SmartVault is run thin at 9% margins to maximise growth ahead of a potential sale. After both segments and £3.7m of central costs, group EBITDA is only £0.3m (1% margin).

The “crown jewel” is SmartVault, a fast-growing US tax-document platform earmarked for sale and, on its own, worth more than the company’s entire EV.

1) SmartVault (57% of FY2025 revenue, 9% EBITDA margin): SmartVault is a tax-focused document-management system and client portal with workflow on top (document requests, e-signatures). This basically means that during tax season, a firm uses SmartVault to request files from a client through the portal, the client uploads them, and the firm keeps and shares everything in one secure place.

Customers are sticky. They stay roughly 10 years, and churn is under 1% a year. ARR was $17.8m at end-2025 and $18.5m by April 2026. This is the business management intends to sell.

2) Workiro / Virtual Cabinet (43% of FY2025 revenue, 30% segment EBITDA margin): Similar to SmartVault, but aimed at the back office rather than US tax prep, and at the UK/Australia/New Zealand market.

Workiro runs inside Oracle NetSuite, the system companies use to run finance and operations, which opens up NetSuite’s 41,000 customers, and it has recently been plugged into TaxCalc (11,000 UK firms).

Workiro is used by 30% of the UK’s top 100 accounting firms. It’s the group’s cash engine (£9.3m ARR, £2.9m EBITDA, 30% margin), but ARR slipped 2%, and EBITDA fell from £3.4m as old Virtual Cabinet customers are migrated onto Workiro and some churn along the way. Management expects a return to growth in 2026.

Reasons to Follow

1) SmartVault is Worth More than the Company’s EV: On May 13, 2026, GetBusy posted a trading update and stated that in April, SmartVault’s ARR was now at US$18.5M and grew by 19%. Based on this number, we can get an idea of how much SmartVault is worth.

If we look at the past Thomson Reuters (TR) acquisitions, we can see that they have paid EV/Sales multiples of 8.0-10.0x.

Note: I intentionally focused on TR’s acquisitions because I think they could buy SmartVault. They’re currently one of Getbusy’s customers.

SurePrep (January 2023): Tax automation software and service company acquired for US$500m in January 2023, about 8.3x its $60m revenue (growing 20%+)

SafeSend (January 2025): Cloud-native provider of technology for tax and accounting professionals acquired for $600m in January 2025, about 10.0x its $60m revenue (growing 25%+).

Even if we cut SmartVault for its smaller size and slightly lower growth rate of 19%, it would probably fetch an EV/Sales multiple north of 5.0x. To put that into perspective, the entire business is trading at an EV/Sales of around 1.7x.

At 5x, SmartVault alone is worth US$92m (5 × $18.5m) / £69m, roughly twice GetBusy’s entire enterprise value of £37m. So the market is pricing the whole company at less than half of what just SmartVault would likely fetch, and handing you Workiro (another £14–23m) for free.

2) Strategic Buyer - Thomson Reuters (TR): A bear case that many of you have probably already been thinking about is: “Why would a company buy SmartVault if they can just build something similar with AI?”

Well, Thomson Reuters owns UltraTax, one of the major US professional tax-prep programs and a direct rival to Intuit’s Lacerte and ProConnect. It’s a serious software builder that can build a SmartVault-style document layer itself. Yet instead, it keeps buying these workflow and document assets (SurePrep, SafeSend) and layering its own AI on top. Its actual playbook is the opposite of “we’ll just build it ourselves”; they are buying the embedded workflow and building the AI on top.

The AI era has only sharpened this. Through 2025, TR went all-in on AI for tax and accounting. It launched CoCounsel, its agentic assistant, and “Ready to Review,” which drafts 1040 returns straight from a client’s source documents. The interesting aspect about this is that TR built all of it on top of the workflow assets it had already bought, using an AI team it had also bought (the Materia acquisition). In TR’s own words, it’s “re-architecting” the products firms already use rather than building standalone tools, and its product chief describes the real moat as “the trusted tools professionals already use daily”, with AI layered on.

TR isn’t a passive bystander here. The recent trading update credits much of SmartVault’s growth to Thomson Reuters and Intuit ProConnect, and TR has a habit of buying the companies it partners with. It resold SurePrep’s software for about six months before acquiring it, and described the Pagero deal as “building on” an existing commercial partnership.

3) Management is incentivized to sell SmartVault: Getbusy and SmartVault management are incentivized to sell SmartVault and then distribute the proceeds through two plans:

Leadership Incentive Plan

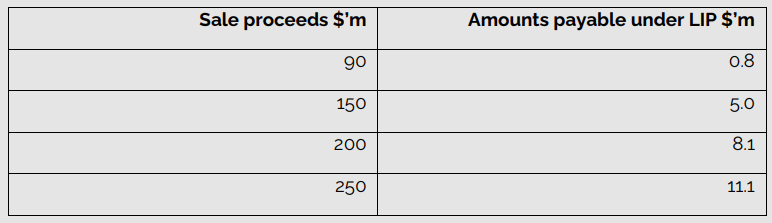

“The LIP rewards certain members of management [SmartVault’s own divisional management] in the event the SmartVault business is wholly acquired by a third party before 31 December 2028. The award starts to become payable at sale proceeds of $90m with a maximum award at sale proceeds of $250m. The table below shows the total amount payable (including estimated social security costs at current rates) at differing levels of sale proceeds:”

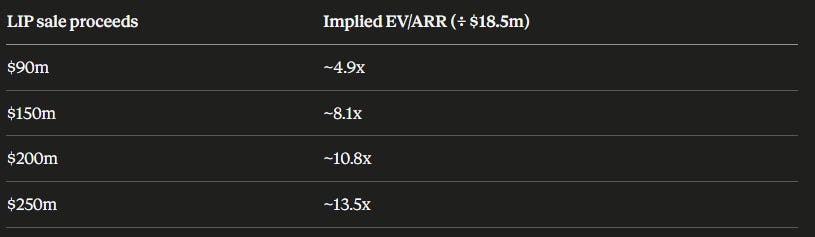

Using the LIP Table, we can get an implied EV/ARR multiple for SmartVault by dividing the sale-proceeds thresholds (US$90m–US$250m) by SmartVault’s most recent $18.5m ARR. The table shows management built the plan around an implied 4.9x to 13.5x multiple, with meaningful money only from US$150m (8.1x) upward.

Implied SmartVault Multiples

This means:

The award starts paying at 4.9x, so management implicitly treats US$90m/4.9x multiple as the floor worth incentivising.

The heart of the payout schedule (US$150m–US$200m, ~8–11x) is exactly where SurePrep (8.3x) and SafeSend (10x) were sold.

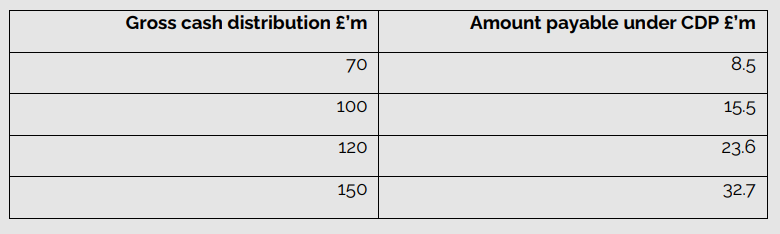

Cash Distribution Plan

The Cash Distribution Plan separately pays GetBusy’s CEO/CFO £8.5m–£32.7m for distributing £70m–£150m of cash to shareholders within seven years of March 2023 (i.e., by March 2030).

In a nutshell, the LIP rewards SmartVault’s own divisional management for selling SmartVault to a third party, and the CDP rewards GetBusy’s leadership (CEO and CFO) for then distributing the cash to shareholders. The two plans pay each team to do exactly what minority holders want: sell the asset, then hand back the proceeds.

In the 2025 Annual Report, management even stated:

“GetBusy is focused on generating material cash returns from SmartVault in the medium term, while building long-term strategic value through AI-enabled workflow platforms...”

4) The SmartVault Inflection: ARR growth re-accelerated from 16% (2025) to 19% by April 2026, with new business up 36%. Management targets 20%+ ARR growth and a step-up to a 20% EBITDA margin from 9%, i.e., the asset is getting bigger and better into a potential sale window.

5) Workiro for Free - A profitable, re-growing downside leg: In 2025, Workiro generated £9.3m in ARR and £2.9m in segment EBITDA. Although Workiro shrank by 2% in 2025, in the latest trading update, management stated that Workiro had returned to growth, but did not give any specific number. We don’t really need Workiro to grow for the thesis to work, but it’s probably worth around £14–23m (1.5–2.5x its £9.3m ARR).

6) Insiders Accumulating: The controlling Rabie family (30%+ combined, worth around £11.1m) bought heavily on the open market through 2025–26 at 64–83p, much of it at or above today’s 73p. That’s striking against modest pay: the CEO earns £271k and Clive, the largest shareholder, takes only a £42k non-exec fee, so the buying dwarfs their salaries.

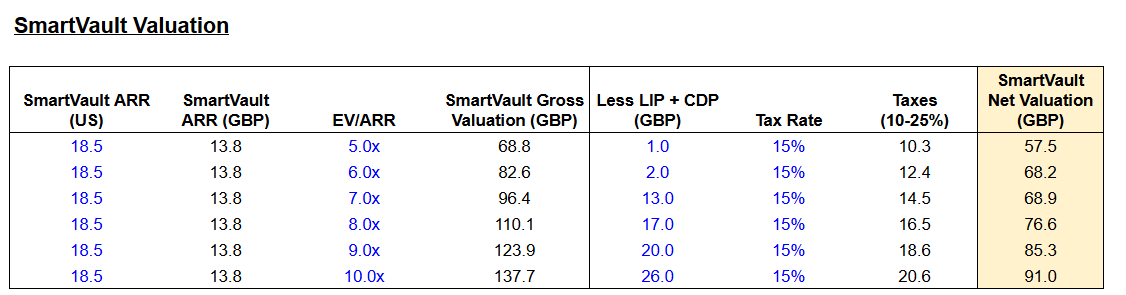

Valuation

This values SmartVault on its own, across a range of sale multiples. Take its current ARR (U$18.5m, £13.8m), apply a 5–10x EV/ARR multiple for a gross sale value, then strip out what wouldn’t actually reach shareholders: the management incentive payouts (LIP + CDP) and tax. The incentives are tiny at low multiples but jump at 7x, that’s where the cash distribution crosses £70m, and the CDP switches on. Tax is held at a deliberately conservative 15%; in reality, it could be far lower (~5%) if the deal is structured as a share sale qualifying for UK Substantial Shareholdings Exemption, or up to ~25% in a less favourable asset deal. Even after both deductions, SmartVault is worth £58–91m net, comfortably more than GetBusy’s entire enterprise value (~£37m) on its own.

I should also point out that this valuation does not assume further SmartVault growth, meaning that if SmartVault continues growing, it’s free upside.

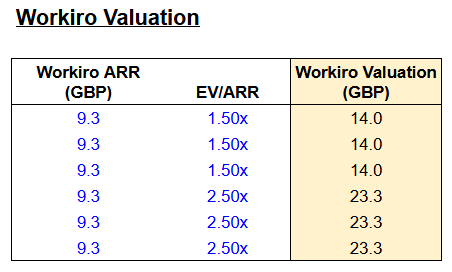

Workiro is the business that stays after a SmartVault sale, so it carries no tax or incentive haircut; shareholders simply keep owning it. It’s profitable (30% segment margin), cash-generative, and slow-growing. The one adjustment: its £2.9m is segment EBITDA, struck before the group’s £3.7m of central cost, so as a standalone Workiro has to shoulder some overhead. If Workiro is itself sold and a buyer absorbs that cost, it’s worth ~2–3x its £9.3m ARR; if it’s held as a standalone listco carrying ~£1.5m of stranded cost, closer to ~1–1.5x (£9–14m). Conservatively, I anchor it at 1.5–2.5x ARR, roughly £14–23m. Either way, the thesis doesn’t need Workiro to grow.

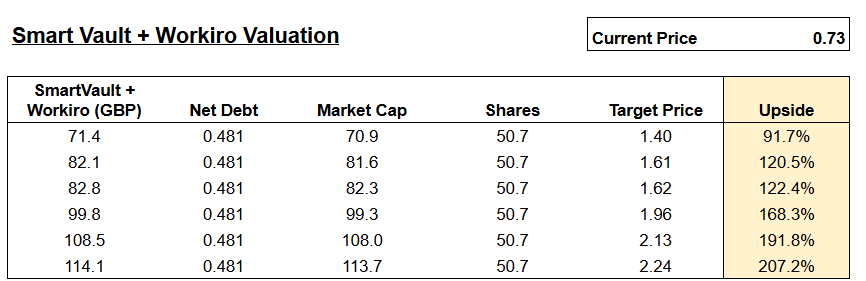

Putting the two together gives the whole company. Add net SmartVault to retained Workiro for total asset value, subtract net debt (£0.5m) for equity value, and divide by 50.7m shares for a target price. The result: a target price of £1.40–£2.24 against today’s 73p, roughly 92% to 207% upside, with a central case (7–8x SmartVault) around £1.62–£1.96, or 122–168% upside.

Note: The assumptions are deliberately conservative because they use Smartvault's current ARR rather than a higher 2028 figure.

Risks

Value realization is the family’s call. Minorities can’t force a sale or a distribution; the controlling Rabie family decides if, when, and on what terms. Their cost of waiting is low (salaries, board control, a compounding asset, and Clive Rabie earns interest as the lender), so the discount can persist for years.

No deal is in motion. No strategic review, no adviser, no Takeover Code announcement, and, tellingly, no capital-reduction or return-of-capital authority anywhere in the AGM notices through 2026. The LIP’s December 2028 deadline is the only clock; if it slips, the catalyst slips with it.

Platform dependency on Thomson Reuters and Intuit. The two giants explicitly drove the recent acceleration, which concentrates SmartVault’s fortunes in players who could change terms, build their own document layer, or displace it. They may also keep capturing the value through partnership without ever buying, capping any exit multiple.

AI cuts both ways. It bites the “no-sale, hold-forever” case hardest, as the document moat erodes over time; on the sale horizon, it may even add urgency for an acquirer to lock in the position. A real risk to the floor, less so to the catalyst.

Research Tasks

Post-sale corporate cost base: The single biggest swing on the rump: does standalone Workiro carry the ~£3.7m central cost, or is most of it stripped out with SmartVault?

Deal structure and tax leakage: The biggest SOTP swing after the multiple, but the key question isn’t just SmartVault’s tax base cost and available losses, it’s whether a sale would be a share sale qualifying for UK Substantial Shareholdings Exemption, which could cut the tax toward zero.

Durability of SmartVault’s growth: How much of the recent acceleration is the one-off Thomson Reuters FileCabinet sunset (finishing 2027) versus durable demand?

The first hard transaction signal: Watch for a capital-reduction circular outside the normal AGM cycle, or a Takeover Code “possible offer” / Rule 2.7 firm-offer RNS. Until one lands, the catalyst is a watch-item, not a fact.

Looks like I can’t get it on Schwab. Maybe if I called in.