[Cliff Note Update]: A Debt-Free, Microcap Compounder with Defence-Tech Optionality

Trading Under 10x Trailing FCF, Growing 25%+, Net Cash Greater than All Liabilities, Free Defense Optionality

Over the past few months, we have begun publishing Cliff Note Updates on stocks already in our Microcap Quality Index. Remember, every time we add a stock to the index, we publish a Cliff Note so you understand why we added it.

The idea for a Cliff Note update is simple: whenever we spot a meaningful development that we believe could materially change a company’s trajectory, whether a new product, an expansion into new markets, or a breakout quarter, we revisit the original Cliff Note and refresh our view.

The goal is to help you navigate our index and surface the strongest opportunities within it.

We believe our goal to create a prime hunting ground for quality microcaps and high-probability turnarounds is playing out nicely.

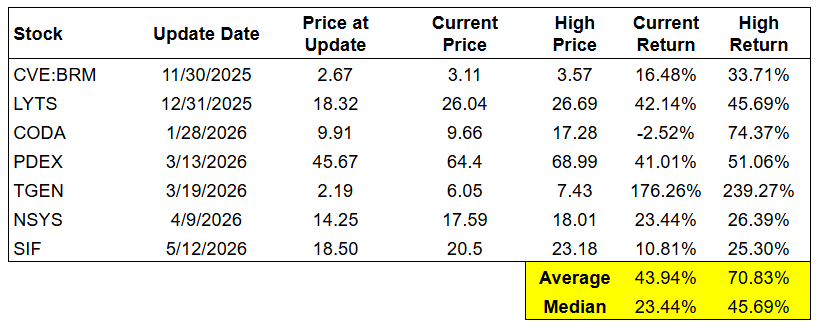

So far, the results of our Cliff Note updates have been encouraging. As the table below shows, these updates have delivered strong returns, especially considering that every one of them has been published within the past year.

Elevator Pitch Related To Our Next Cliff Note Update

This is a profitable, debt-free, non-dilutive nano-cap that the market still prices like a sleepy hardware reseller, not the cash-generative compounder it has quietly become.

Screen it on P/E, and you will walk right past it: at around 20 times earnings, it looks ordinary. But P/E is the wrong lens here.

Strip out a fortress net-cash balance sheet and look at what actually matters… free cash flow and the same business is changing hands for under 10 times trailing FCF.

You are paying a fair price for today’s profits and getting the growth of more than 25% growth over the last few quarters, the recurring revenue, and the optionality thrown in for free.

The optionality is the real prize. The company’s core sensing platform has already been adapted for security and border-surveillance use and is in a small, paid government field trial. This avenue can feed both one-time hardware sales and high-margin recurring revenue, in a market where governments are spending heavily. The market assigns this opportunity exactly nothing today.

If even one of those trials converts into a real contract, this re-rates from a forgotten micro-cap into a profitable, growing platform with a defence leg, and you will already know it before anyone is looking.

See the idea below…