Ask Who Management Respects

Lynch found La Quinta by asking a rival who they feared. Here's how I run the same play across PPIH, TGEN, CGEH, MIND, KLNG, KTEL, and the rest of my book.

A few weeks ago, @TheBigBerbowski posted a tweet referencing a part of Peter Lynch’s book, One Up On Wall Street, that brought back memories.

Lynch talks about the benefit of asking management questions about the competition, but more specifically, who they respect the most.

Once in a while, you’ll come up with a name you hadn’t been tracking or will learn more about a comp you already had on your list. Best unpaid research you’ll ever get!

The passage Berbowski was referencing was when Lynch was interviewing a motel company, and La Quinta Inns came up:

I vividly recalled this section of the book, as it helped shape part of what I ask management during my conversations with them. It sounds like a simple and obvious thing to do, but some of you might feel intimidated or kind of weird asking that question, like maybe it’s offensive.

However, it’s a great approach, and I took Lynch’s advice literally.

I used to count cars in parking lots, ask the restaurant staff how business was trending, or ask if they were happy, and stalk mall retail stores and their customers.

Unfortunately, that’s when I discovered my favorite fast food joint, Chick-fil-A, and learned they’d never go public. Imagine if you could have bought stock in 1988! The company has expanded by roughly 8x in store count and by nearly 100x in sales (from $232 million in 1988 to over $20 million today).

Anyways, I wanted to lay out a few examples to show how I’ve expanded on this research process by using stocks I own(ed) and have written about in this substack…

Competitive Positioning: TGEN vs. CGEH

I currently own both $TGEN and $CGEH, two microcaps that both have a stake in the AI data center buildout, but from different angles. While TGEN sells cogeneration power and cooling solutions, its current opportunity is its gas-engine chillers that offload cooling from the electrical grid at peak power conditions, freeing up electric power for computing (a data center’s revenue driver).

CGEH makes microturbines that mainly serve as a distributed power generation source, reducing dependence on the grid entirely.

Basically, TGEN is not trying to necessarily compete in CGEH’s power generation solution areas, although it is possible that CGEH might be trying to compete in some of TGEN’s cooling use cases.

So they’re not pure competitors, but they’re fishing in the same pond, maybe pitching to the same data center operators, for budget from the same capital allocation decision.

So I asked each CEO about the other. What I wanted to know wasn’t just what they thought about overall competition, it was also whether they had a clear-eyed view of where their own value proposition began and ended, including vs. each other. Basically, to confirm what I generally already knew.

Interestingly, I learned that in some instances, the two companies could actually be complementary, maybe setting up for a channel partner relationship. For example, I could see them working together to pitch a more complete solution to a data center.

Talking to both teams also helped me interpret an expert call I came across, where an investor was trying to understand the competitive advantage positioning of both companies, but mainly TGEN. I felt that I knew more than the investor and hyperascaler expert on the call, enabling me to internally counter some of the slightly inaccurate comments the expert made during the call about TGEN’s competitive positioning and use case topics.

He just didn’t get how TGEN’s solution has significant competitive advantages when a data center has reached peak power conditions. Although TGEN does have power solutions, it isn’t necessarily positioning itself to address the entire data center power problem. Its focus is targeted and unique, which is why I love it.

However, it amazes me how many people just don’t understand this, even though the CEO repeatedly goes over it on earnings calls. I was waiting for the expert to pound that home. He just didn’t get it. It’s like I wanted to jump through the transcript and smack him in the face. Because now you have all these investors reading this transcript and interpreting it wrongly. Well, there you go, I went off on a tangent again.

On a sidenote, this also shows that you just can’t blindly listen to these expert calls and assume they’re totally accurate.

It also made me feel a little more comfortable about the explanations that the CEO of TGEN gives on earnings calls on why it’s taking them a little longer to close a major data center deal. If a hyperscaler expert working in the industry doesn’t quite understand everything about the clear value proposition, then there’s going to be a learning curve.

TGEN is in our microcap quality index

I own a significant amount of TGEN and a small amount of CGEH.

Competitive Positioning: MIND vs. KLNG vs. CODA

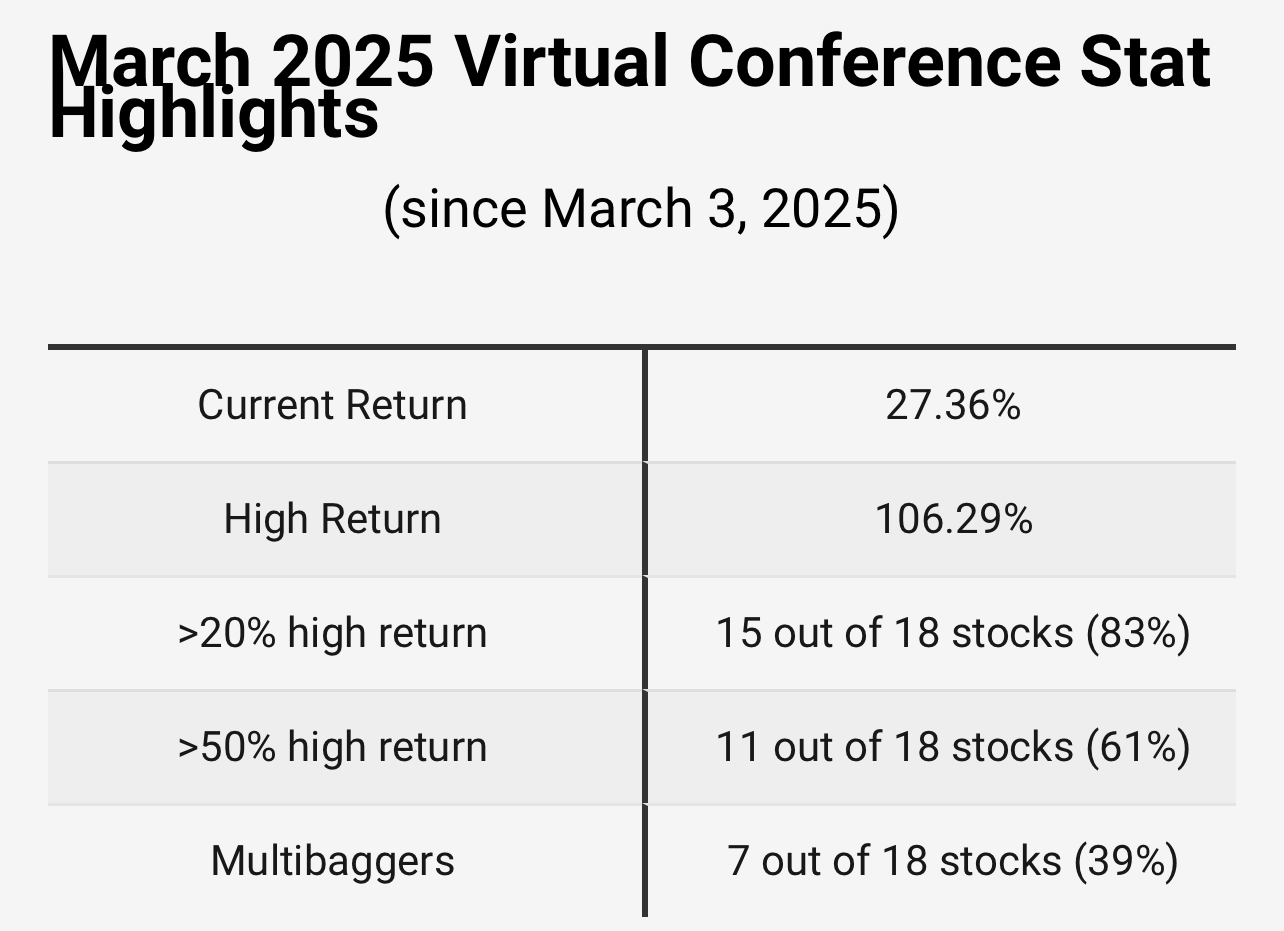

In early March 2025, we hosted a virtual conference marathon over 5 days, where both KLNG and MIND presented.

You can view all the presentations here

By the way, I just looked at the conference stats… not earth-shattering, but certainly not bad, when you consider 18 companies presented.

KLNG and MIND both compete in the subsea industry. I saw this as an opportunity to ask them both about the competitive landscape and if they actually competed against each other, or if channel partner opportunities between them existed. Then, I could cross-check their answers in real-time. I also threw some subsea players, CODA, and PNG.V (KRKNF: OTC) into the mix.

Hats of to Short & Squeeze Corner and Tomek Hill for their MultiBagger pitches on PNG.

MIND, KLNG, and CODA are all in our microcap quality index. PNG was included in one of our research pipeline updates due to Sean’s and Tomek’s contributions.

It was interesting to see that MIND and KLNG management had the same conclusion, in that they didn’t really see meaningful competitive overlaps. They are at different parts of the value chain. I was kind of relieved because at the time, I owned both companies.

I currently only own KLNG, based on increased visibility for the first time in years, due to large multiple contract awards. This should allow them to post some nice revenue growth across several quarters. I’m still waiting on margins to inflect. However, the lower margins are partly due to the company making investments in its rental business, which should eventually lead to recurring revenue, more predictability, and higher margins.

I owned MIND for a short period of time and made some good money in the stock. However, they just can’t seem to offset the lumpy nature of their business, even though 50% of the business is from recurring maintenance types of contracts.

CODA is just a hot mess and has not been able to deliver on its new mapping/analytics product launch goals for years. If they can get their new smart diver goggles to gain order momentum… now that the goggles are certified by the Navy… it gets interesting. I own a very small amount of CODA.

Uncovering Biz Dev Possibilities: ATGN, KTEL, CXDO

An underappreciated dimension of understanding competition goes beyond what it does for your research. It’s also what it can do for your portfolio companies. When I got a deep enough understanding of two cloud communication software companies I own, $KTEL and $ATGN, I realized connecting them could create real value, which resulted in revenue for one and cost savings for the other. Unfortunately, the economic significance is probably not meaningful at this point, but we’ll see if it grows. The point is that I found a way to potentially help my own portfolio by connecting companies. To put it simply, KTEL was able to offer connectivity solutions to ATGN at a better price point than the popular vendor it was using for that solution.

I recently did the same thing, connecting KTEL and $CXDO, due to both having POTS replacement operations.

I currently own a small amount of CXDO.

For those interested:

POTS replacement is a multi-year effort to replace aging copper phone lines with cellular and IP-based solutions. Millions of legacy devices, including alarm systems, elevators, and fire panels, still depend on these lines, creating a significant upgrade cycle for vendors serving the market. Basically, the FCC has lifted pricing restrictions that are enabling telecom companies to accelerate this “movement” so they can start replacing costly copper line infrastructure with more modern infrastructure.

By the way, this is a huge opportunity that I think investors might be underappreciating for both companies. The biggest obstacle for both of them is how to scale the POTS replacement business, since there are some initial installation CAPEX requirements.

I’ve actually formalized this biz dev framework into a rough grid to help me see if I can build business development connections across more companies that I own or already follow. It maps each stock to its connection points, like competitors, channel partners, customer overlaps, and technology adjacencies. Each node generates new branches. A stock you own might connect to a competitor you don’t own yet. That competitor’s customer turns out to be a company in your portfolio. The tree just keeps building itself.

Two Final Examples:

With $PPIH, one of my top five favorite companies I own right now, I’m currently attempting to verify some of their competitive “moat” product claims. This is taking me down a rabbit hole of not just understanding what they do, but deep into the supply chain.

The CEO of another stock I own told me that he decided not to beef up his marketing staff to drive sales on $AMZN … instead choosing to spend a few hours just mirroring the way the leading competitor set up its AMZN pages (and it worked).

Both of these last two stocks are in our microcap quality index. I own them both.

Well, that’s a wrap. If you have any company that you believe has a business development opportunity with its competitors or other public companies, please let me know. I would love to help you accelerate these connections, especially if it helps grow your portfolio.

Interesting write up. I'm relatively new. What are your other 4 top picks?